The Hidden Asset in Warner Bros Discovery's Sale: Gaming IP Worth Billions

The winner of the Warner Bros Discovery sweepstakes will get far more than an IP catalog and over 100 million streaming subscribers.

Dear Readers,

Everyone analyzing the inevitable Warner Bros Discovery acquisition is focused on the obvious assets: the streaming platform with its HBO prestige content and the studio’s century-old film library. Meanwhile, Wall Street debates whether to value the declining cable TV business as an asset or liability.

But there’s a strategic asset hiding in plain sight that could determine which buyer wins and what they pay: Warner Bros’ gaming division and its catalog of billion-dollar franchises.

Yes, WBD’s gaming division has taken a brutal beating over the past 18 months. According to WBD’s Q1 2025 earnings report, gaming revenue fell 48% compared to the same quarter a year earlier. This follows a disastrous 2024 that saw the company write off $384 million in gaming losses, with Suicide Squad: Kill the Justice League losing $200 million and MultiVersus hemorrhaging another $100 million.

But here’s what the headlines miss: despite these catastrophic failures, WBD’s studios segment—of which gaming is integral—generated $3.4 billion in revenue in 2024. More importantly, each of WBD’s four tentpole gaming franchises (Harry Potter, Game of Thrones, Mortal Kombat, and DC) has generated over $1 billion in lifetime revenue.

WBD still considers gaming to be a “strategic differentiator” that is key for “long-term consumer engagement.” They’re right.

And for the companies circling this acquisition, the gaming IP might be more valuable than the streaming subscribers everyone’s counting.

Why Gaming Makes or Breaks This Deal

The entertainment industry has finally figured out what savvy operators knew years ago: gaming isn’t just another revenue stream—it’s the engagement engine that makes everything else work.

Gaming delivers what streaming and theatrical can’t: sustained, interactive engagement with IP that builds emotional investment and extends franchise value across decades rather than weeks. A successful game keeps players engaged for hundreds of hours, creating deeper connections to characters and worlds than passive viewing ever could.

PwC’s Global Entertainment & Media Outlook 2024 projects gaming will reach $321 billion by 2027, but the real value isn’t in gaming revenue alone—it’s in how gaming amplifies the value of entertainment IP across all channels.

Consider the Marvel Cinematic Universe: Marvel’s Avengers game may have lost money, but Marvel’s Spider-Man generated $3.8 billion in revenue while reinforcing the character’s cultural dominance and driving merchandise sales that dwarf gaming revenue.

WBD’s restructuring into focused studios—Warner Bros. Games Montreal handling Harry Potter and Game of Thrones, NetherRealm Studios managing DC and Mortal Kombat, and Warner Bros. Games New York overseeing publishing—demonstrates they understand gaming requires specialized expertise and long-term investment, not Hollywood’s traditional hit-driven approach.

For any acquirer, the question isn’t whether WBD’s gaming division is currently profitable. The question is what an acquirer with the right strategy and resources could do with billion-dollar franchises like Harry Potter, Game of Thrones, DC, and Mortal Kombat.

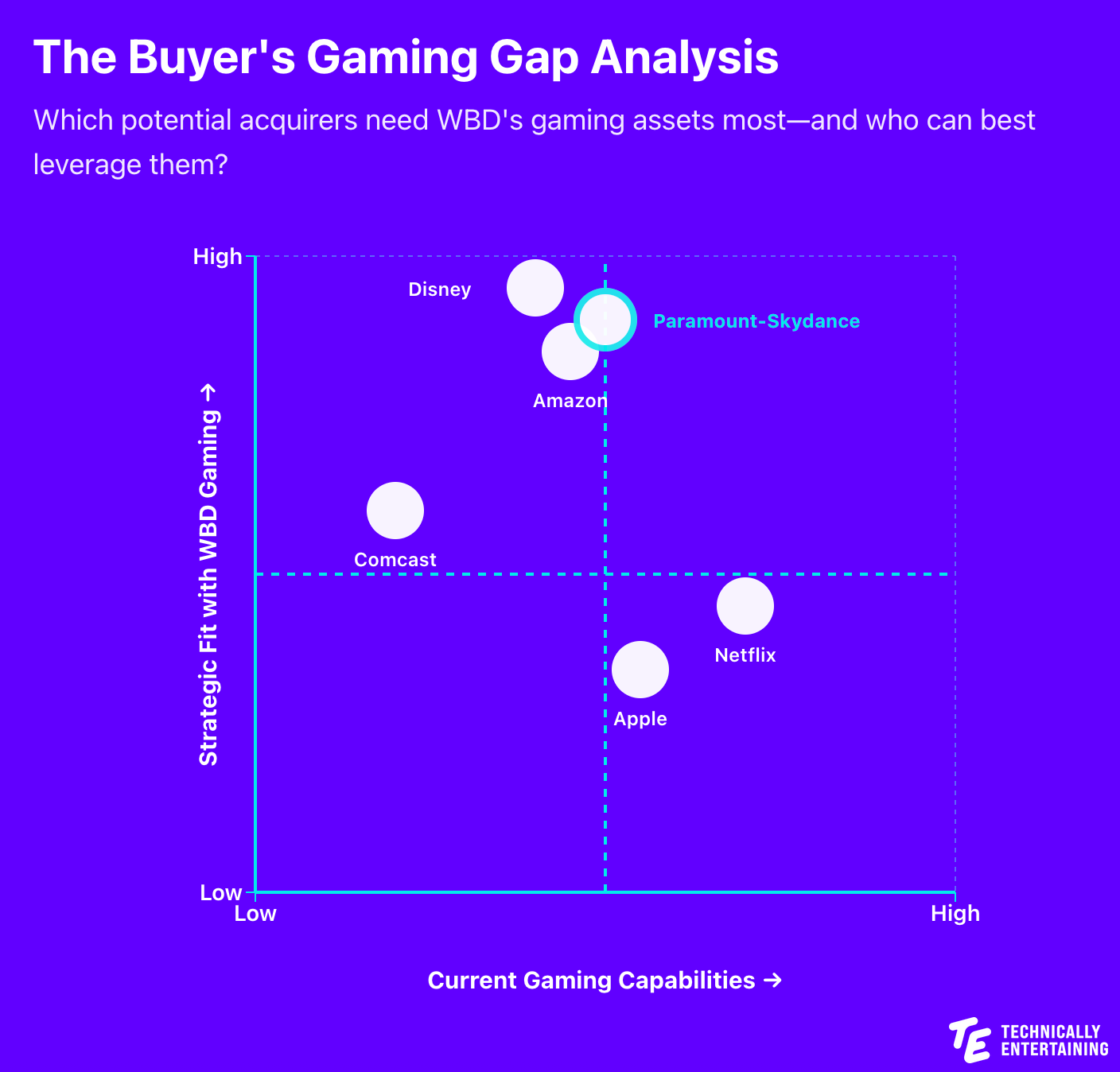

The Buyers and What Gaming Means to Each

Paramount-Skydance: The Strategic Transformation Play

Likelihood: High

For David Ellison’s newly combined Paramount-Skydance, acquiring WBD would be transformational—and gaming would be the linchpin of that transformation.

Skydance already has gaming DNA through Skydance Interactive, which has developed successful VR titles. The same is true for Paramount via Paramount Game Studios and Paramount Digital Entertainment. More importantly, they understand that the future of entertainment companies isn’t about owning distribution channels—it’s about owning IP that can generate revenue across multiple consumer touch points.

The combination would be powerful: Paramount’s Star Trek, Mission: Impossible, and Transformers franchises combined with WBD’s Harry Potter, Game of Thrones, DC, and Mortal Kombat. With Oracle’s infrastructure backing from Larry Ellison, Paramount-Skydance could build the cloud gaming and live service capabilities that WBD’s games desperately need.

The strategic fit is obvious. Paramount-Skydance is building toward a transmedia future where content flows seamlessly between films, streaming, games, and consumer experiences. WBD’s gaming franchises, properly resourced, could become the engagement layer that makes this vision work.

Gaming synergies: Immediate access to four billion-dollar franchises, existing development studios with franchise expertise, and the ability to cross-pollinate IP between Paramount and WBD properties. Imagine a Harry Potter game using Skydance’s VR expertise, or a Game of Thrones title built on Oracle’s cloud infrastructure for massive multiplayer experiences.

Comcast: The Cable Hedge

Likelihood: Medium-Low

Comcast faces the same existential threat as WBD: cord-cutting is accelerating and traditional cable is dying. According to Comcast’s Q4 2024 earnings, they lost 490,000 video subscribers in the quarter alone.

For Comcast, WBD’s gaming assets represent a hedge against declining cable revenue and a way to differentiate Peacock in an increasingly crowded streaming market. But here’s the critical challenge: Comcast has virtually no gaming development expertise. They own Universal’s gaming partnerships—licensing deals where others develop the games—but they’ve never built or operated game studios.

This creates massive execution risk. Gaming requires specialized talent, patient capital, and cultural acceptance that creative processes don’t follow predictable timelines. Comcast would be acquiring four game studios and billion-dollar franchises with no internal capability to manage them effectively.

The strategic logic is sound—gaming gives Comcast a direct consumer relationship that doesn’t depend on distributors, and theme park integration opportunities are obvious. But Comcast would need to completely trust WBD’s existing studio leadership rather than imposing traditional media company processes that would destroy value.

Gaming synergies: Theme park integration for Harry Potter (competing directly with Disney’s offerings), Peacock gaming content and interactive experiences, cross-platform bundle opportunities. The Universal and WBD IP libraries combined could create a legitimate third pole in gaming franchises. But success depends entirely on Comcast’s willingness to operate gaming as a separate business with different rules than cable or streaming.

Amazon: The Everything Store Wants Everything Entertainment

Likelihood: Medium

Amazon’s strategy has always been about owning customer relationships and selling them everything. Gaming fits perfectly into that vision, especially as Amazon continues building out its entertainment ecosystem through Prime Video, Twitch, and Amazon Games.

Amazon’s gaming efforts have been mixed—New World found an audience, but multiple canceled projects and studio closures show they’re still figuring out gaming. WBD’s established studios and proven franchises would solve Amazon’s biggest gaming problem: they have distribution (Twitch) and infrastructure (AWS) but lack the IP and development expertise to create blockbuster games.

The integration could be powerful. Amazon could leverage AWS for cloud gaming infrastructure, use Twitch for marketing and community building, and integrate games with Prime membership benefits. WBD’s franchises would get Amazon’s patient capital and infrastructure while Amazon gets the gaming credibility and consumer engagement they’ve been chasing.

Gaming synergies: AWS-powered cloud gaming for WBD titles, Twitch integration for live content and esports, Prime Gaming bundle opportunities, and Luna cloud gaming service finally getting premium content. Amazon could also leverage WBD’s games for Alexa integration and smart home experiences, extending gaming beyond screens.

Netflix: The Engagement Problem

Likelihood: Medium-Low

Netflix’s existential challenge is that streaming has become commoditized. Content libraries are similar, originals are expensive, and subscribers churn the moment they finish their latest binge. Netflix’s gaming push has been more substantial than many realize—they’ve built significant mobile gaming capabilities and acquired multiple studios.

Here’s the paradox: Netflix has surprisingly strong gaming capabilities—they’ve invested heavily in mobile gaming infrastructure and talent. But WBD’s gaming assets don’t align with Netflix’s mobile-first strategy. Harry Potter, Game of Thrones, and DC aren’t mobile puzzle games—they’re AAA console and PC franchises that require completely different expertise and go-to-market strategies.

The challenge: Netflix has the gaming talent but the wrong gaming strategy for WBD’s assets. They’d be buying expensive AAA studios and billion-dollar console franchises when their entire gaming playbook is built around mobile experiences bundled with streaming subscriptions.

Gaming synergies: Netflix could theoretically pivot their gaming strategy to AAA titles, integrate WBD games into their streaming interface, and build a legitimate gaming subscription service. But this requires Netflix to fundamentally rethink their gaming approach—a strategic U-turn that seems unlikely given their mobile-first investment thesis.

Apple: The Ecosystem Play

Likelihood: Low

Apple’s gaming relationship is complicated. They make billions from the App Store’s 30% cut of mobile gaming revenue, but they’ve shown little interest in developing or publishing games themselves. Apple Arcade has been modest, focusing on premium mobile experiences rather than blockbuster franchises.

WBD’s gaming assets would give Apple instant credibility in AAA gaming and exclusive franchises for Apple Arcade+. Combined with Apple’s hardware ecosystem, cloud infrastructure, and retail presence, they could create a closed-loop gaming ecosystem that rivals Sony and Microsoft.

But Apple’s culture works against this. They prefer to control platforms and take cuts from others’ content rather than investing heavily in content creation themselves. Gaming studios require patient capital, tolerance for failure, and cultural acceptance that not every project will hit Apple’s quality standards.

Gaming synergies: Exclusive AAA titles for Apple platforms, integration with Vision Pro for VR experiences, Apple Arcade+ premium tier with WBD franchises, and retail presence for physical game merchandise. Apple could also leverage gaming to drive hardware sales—imagine Harry Potter or DC games optimized for Mac gaming.

Disney: The Unlikely Reunion

Likelihood: Very Low

Disney and Warner Bros have circled each other for decades, but regulatory scrutiny would make this deal nearly impossible. Disney already faces antitrust pressure, and adding WBD would give them an unprecedented concentration of entertainment IP.

From a gaming perspective, Disney presents an interesting paradox. Their gaming capabilities are modest—they famously shut down Disney Interactive Studios in 2016 and have since relied on external partners for Marvel and Star Wars games. They have gaming expertise through these partnerships but no in-house AAA development capability.

Yet the strategic fit is undeniable. WBD’s studios would give Disney the in-house gaming capability they’ve lacked for years while adding Harry Potter and Game of Thrones to their already dominant franchise portfolio. Combined Marvel/DC gaming, Star Wars competing with Game of Thrones in fantasy gaming, and theme park integration would create unprecedented synergies.

But regulatory reality makes this impossible. The concentration of entertainment IP—Disney already owns Marvel, Star Wars, Pixar, and 20th Century Fox—means antitrust regulators would almost certainly block any attempt to add Warner Bros’ DC, Harry Potter, and Game of Thrones franchises.

Gaming synergies: Combined Marvel/DC gaming universe, Star Wars competing with Game of Thrones in fantasy gaming, theme park integration across properties, and Disney+ gaming content hub. This would create a gaming empire that dwarfs anything Sony or Microsoft could assemble. But it’s a fantasy that regulatory reality won’t allow.

The Strategic Reality

WBD’s gaming division isn’t the headline asset in any acquisition discussion—streaming subscribers and content libraries dominate valuations. But gaming might be the strategic differentiator that determines which buyer succeeds.

The buyer landscape breaks down clearly:

Paramount-Skydance leads the pack with the best combination of gaming capability (through Skydance Interactive) and strategic fit. Their transmedia vision, Oracle infrastructure backing, and focus on IP-driven engagement make them the natural fit for WBD’s gaming franchises.

Amazon offers a close second with strong strategic alignment and sufficient capability. They have the infrastructure (AWS, Twitch) and patient capital but need the proven IP and studio expertise that WBD provides.

Comcast desperately needs gaming to hedge against cord-cutting, but their lack of gaming development expertise creates execution risk. They’d be betting on WBD’s existing teams to succeed without the knowledge to manage them effectively.

Netflix has surprisingly strong gaming capabilities but the wrong gaming strategy. Their mobile-first approach doesn’t align with WBD’s AAA console franchises, creating a strategic mismatch despite technical capability.

Apple has gaming infrastructure but low strategic need. WBD’s gaming assets don’t meaningfully advance Apple’s platform-first business model.

Disney would be perfect strategically but faces insurmountable regulatory barriers. Their modest gaming capabilities combined with regulatory impossibility takes them off the board.

The buyer who understands that gaming isn’t just another content vertical—but the engagement layer that makes everything else more valuable—will pay more and win more from the acquisition. That buyer is most likely Paramount-Skydance, with Amazon as a strong alternative if they’re willing to make the cultural changes required to succeed in gaming.

WBD’s gaming disasters of 2024 might actually help any acquirer. The write-offs and restructuring have cleared out the failures and refocused the division on proven franchises. The studios are leaner, the strategy is clearer, and the IP is still worth billions.

The question isn’t whether WBD’s gaming assets are valuable. The question is which buyer understands how valuable they could be in the right hands.

The Warner Bros Discovery acquisition will reshape Hollywood’s competitive landscape. Subscribe to Technically Entertaining for ongoing analysis of the deal dynamics and strategic implications for the entertainment industry and the major disruptions gaming and technology are driving.