The 27-12-10 Problem: Why Brand Leaders Are Behind the Eight Ball on Mobile Gaming in 2026

Only 10% of marketers advertise in mobile games despite 54% of Americans playing them regularly. Mobile games are the blind spot that's costing brands valuable market share.

As I’m preparing for my keynote speech next week at the inaugural iicon conference, bringing together gaming, entertainment, and brands, to talk about why every company needs a gaming strategy to reach modern day consumers, EMARKETER dropped a new report that highlights everything that brand leaders get wrong about their marketing mix and the role gaming plays. The usual suspects still receive the bulk of the marketing budget: CTV, social media, etc.

Games are still an afterthought. They shouldn’t be.

The gap between where consumers actually spend their time and where brand leaders deploy their budgets is now the single largest strategic blind spot in modern marketing. And that gap is widest in mobile gaming.

The report from EMARKETER and Admazing, published last month, lays out the disconnect in numbers that should make every marketing leader uncomfortable. I’ve been writing about the gaming opportunity for years. This study finally puts the math on the table. It shows marketing leaders still haven’t got the memo.

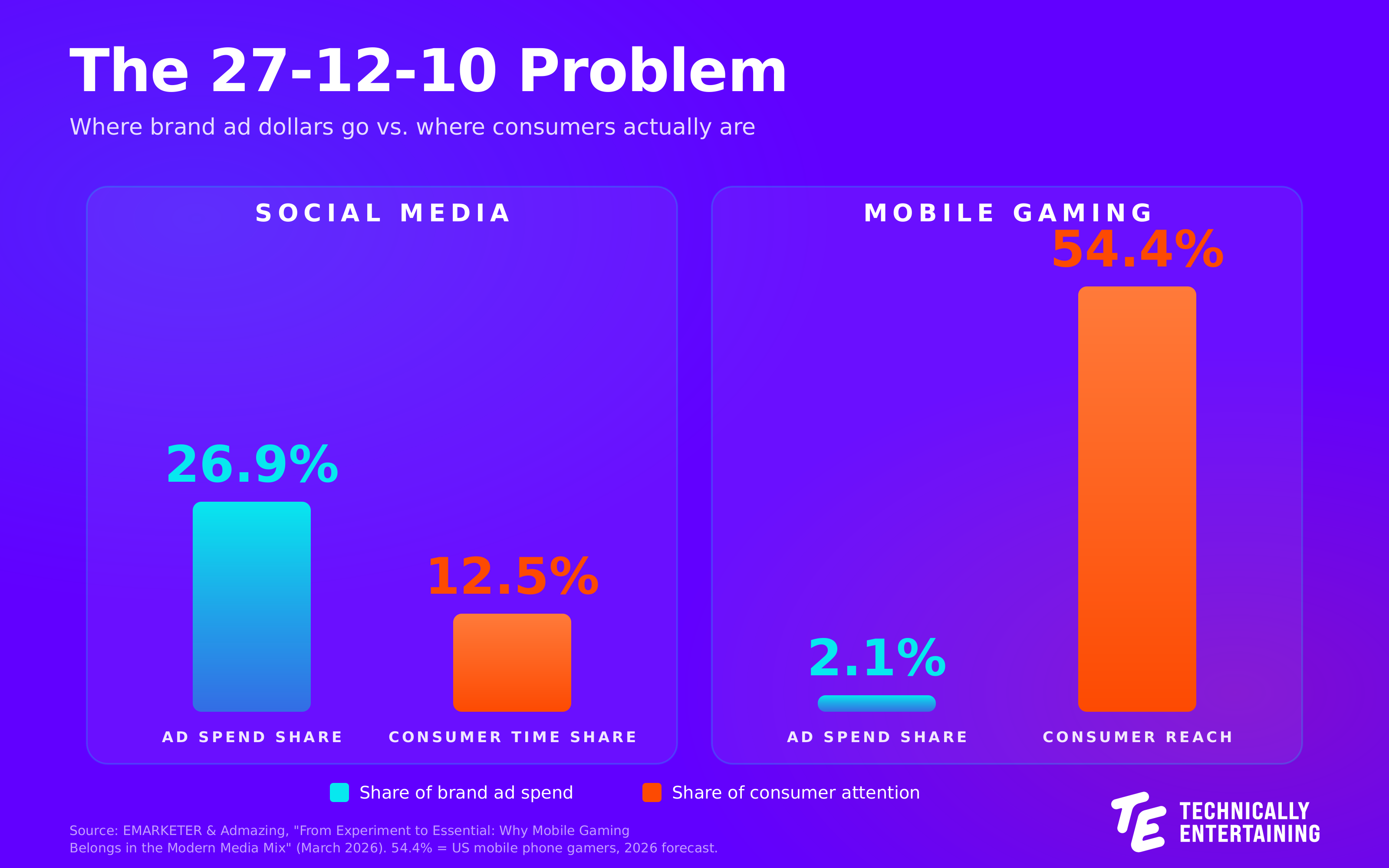

The 27-12-10 Problem

Let me give you three numbers that, placed side by side, tell the whole story of why most brands are behind the eight ball on gaming.

First: 26.9%. That is the share of total US media ad spend going to social networks in 2026, according to EMARKETER. Out of $463.93 billion in projected total US media ad spend this year, roughly $124.88 billion is headed to Meta, TikTok, X, Snap, LinkedIn, and Pinterest.

Second: 12.5%. That is the share of total time consumers spend on social platforms relative to all their media consumption. EMARKETER expects that gulf to widen.

Third: 10.2%. That is the percentage of marketers who say their organizations regularly use mobile gaming for brand campaigns. One in ten. The other nine sit somewhere on a spectrum of inaction: 37.0% rarely consider it, 28.7% deprioritize it in planning, and over a third of B2B/B2C marketers neither use nor actively consider mobile gaming at all.

Put those three numbers together and the picture is clear. Brands are allocating more than double their audience’s actual attention share to social. They are leaving the channel where the audience increasingly lives almost completely alone.

More than half of the US population, 54.4% according to EMARKETER’s October 2025 forecast, will be a mobile phone gamer in 2026. Mobile gaming is a mass medium. It reaches more Americans than Netflix. More than the NFL. More than any single social platform.

Only 2.1% of total digital ad spend is flowing to it.

Why Brand Leaders Keep Missing This

I have had versions of this conversation with dozens of CMOs, brand directors, and heads of strategy over the past year, at Cannes, at Advertising Week, in private client workshops. The reasons brand leaders stay on the sidelines fall into three categories, and each of them has become outdated.

The first is perception. A lingering assumption, rooted in the early 2010s, pictures gamers as a narrow demographic of young men playing hardcore console titles. That picture has been wrong for at least a decade. Candy Crush, Royal Match, Coin Master, Roblox, and Monopoly Go pulled mobile gaming into the mainstream. Yory Wurmser, Principal Analyst at EMARKETER, put it plainly in the report: “Most people in this country are gamers, as are the majority of internet users worldwide.”

The second is historical measurement weakness. This one had teeth. When Apple rolled out iOS 14.5 in 2021 and deprecated the IDFA, the mobile gaming ad ecosystem effectively had its tracking infrastructure cut off at the knees. Attribution, audience signals, and campaign measurement all took a hit. For two or three years, even marketers who wanted to lean into gaming struggled to prove it worked.

The third is budgetary inertia. Media mix decisions are rarely made from scratch. Last year’s plan becomes this year’s starting point, and social and CTV are already locked into the template. Gaming stays out of the conversation because it was out of last year’s conversation. Only 28.7% of marketers even consider mobile gaming alongside core channels, per the EMARKETER/Admazing survey. The rest treat it as optional, experimental, or invisible.

All three of those reasons have collapsed.

The Measurement Argument Is Over

The biggest structural objection to mobile gaming was always measurement. That objection has been retired.

Last year, the Interactive Advertising Bureau released its Gaming Measurement Framework, giving the industry its first standardized benchmarks for in-game ads, rewarded ads, and interstitial ads. Kantar, Circana, DISQO, and the MRC-accredited measurement vendors have all invested heavily in gaming-specific brand lift and outcomes lift methodologies. The ecosystem has matured.

The results these new tools are producing should stop any skeptical marketing leader in their tracks. Pedro Sánchez López, Senior Director of Brand and Media at Kantar, shared a stat in the EMARKETER report that deserves to be printed on a poster in every CMO’s office: mobile gaming ad campaigns deliver purchase intent 3.5 times stronger than the US norm, with a 7.1 percentage point lift.

Three and a half times the purchase intent lift of the US norm. Let that sink in.

López also tracked a shift I have been seeing anecdotally for years. Consumer receptivity to gaming ads has moved from 25% in 2012 to 54% in 2025. The audience welcomes the ads, provided the ads fit the gameplay moment (the second part - authenticity - is crucial and something most brands get wrong).

Erika Digirolamo, Vice President of Media Solutions at Circana, framed the measurement evolution directly. Measurement quality in mobile gaming has moved from basic awareness and engagement metrics to reliably connecting ad exposure to incremental business outcomes. Circana, Kantar, Nielsen, and ComScore now measure mobile gaming with the same rigor they apply to CTV and linear television.

Attention quality, the metric that has become the new currency of brand media, is where mobile gaming outperforms. 86.1% of marketers in the EMARKETER/Admazing survey called attention quality at least moderately important. Mobile gaming, particularly rewarded video, is engineered for attention. The player opts in. The player receives value. The player watches. Rewarded ads landed as the top-performing format in the survey, with 40.7% of marketers naming it their most successful mobile gaming format.

AI Is Closing the Gap Faster Than Brands Are Catching Up

The measurement argument has closed. The creative argument is closing next.

Generative and agentic AI tools are collapsing the production cost of gaming-native creative. Historically, a brand that wanted to show up in a mobile game needed bespoke creative for playables, rewarded video, and interstitials. That investment made gaming feel like an expensive side quest for most marketing teams.

Eddy Prado, Co-Founder and Chief Product Officer at Admazing, described the shift: “AI is helping mobile gaming align with the standards brand marketers expect: clearer measurement, faster creative iteration, and more disciplined budget allocation.” Wurmser echoed the point from the EMARKETER side. Dynamic creative is getting better and cheaper, and personalization at scale has arrived.

Pair that with what AI is doing on the game development side. Studios are shipping more finely tuned titles faster, which means more inventory. More inventory with better targeting and dynamic creative produces a flywheel. The early brands to scale up their gaming buys are about to have a compounding advantage over the ones still treating the channel as experimental.

The Leaders Are Already In

Some brand leaders are already on the right side of this curve. Wendy’s has spent years building presence inside Fortnite and Twitch, showing up where their Gen Z audience actually is. Walmart and Nike launched experiences inside Roblox that reached tens of millions of young shoppers. Hasbro has leaned into Monopoly Go as a billion-dollar IP extension. Mattel licensed Barbie into Roblox and mobile titles ahead of the movie launch. Chipotle, Chevrolet, Coca-Cola, and Stanley have all run in-game campaigns in the past 18 months, and the measurement reports coming out of those campaigns are what is driving the renewed conversations I am having in boardrooms this year.

The CPG category is waking up fastest, which makes sense. Wurmser captured the thesis for that category in one sentence in the report: “Most gamers also do a lot of the shopping for their household. CPG, grocery, and even home improvement advertisers could find opportunities as games improve their targeting and measurement.”

46% of mobile game players regularly make in-game purchases triggered by in-game ads, according to a May 2025 Bain and Company survey. These are active commerce moments inside a premium attention environment.

Your Game Plan, If You Run Marketing at a Consumer Brand

If you are running marketing, brand, or strategy at a meaningful consumer-facing business, here is what I would do this quarter.

Audit your media mix against actual consumer attention. If your share of spend on social exceeds your target audience’s share of time on social by more than 10 percentage points, you have a misallocation problem. Name it and fix it.

Carve out an incrementality test budget for mobile gaming, somewhere between 3% and 5% of your digital spend. Leverage tools like Solsten to understand what mobile games your target audience already plays, and how to best show up this in those environments. Partner with a measurement provider like Kantar, Circana, or Nielsen to run a proper brand lift and outcomes lift study against your existing social and CTV buys.

Prioritize rewarded video and playable formats for your first wave. They carry the attention quality and creative flexibility that travel cleanly from your existing brand campaigns. Depending on your games of choice, pick a partner. Overwolf and Superleague Gaming are great options.

Build an AI-native creative pipeline for gaming. If you are still commissioning gaming creative the way you commissioned a TV spot in 2015, you are leaving the compounding returns on the table. Lean into tools like Elaris that has helped brand leaders increase conversion rates for in-game ads by up to 50%.

The brands that move in 2026 will establish a beachhead before mobile gaming ad inventory gets repriced upward. The ones that wait will pay more for the same audience in 2028.

The disconnect between where consumers spend their time, attention, and dollars, and where brand leaders deploy their budgets, has become indefensible. The data is on the table. The measurement tools are in the market. The audience is waiting inside the games.

The question isn’t whether brands need to shift their budgets to gaming. The question is who will move the fastest and with the most conviction.

Are you meeting your consumers where they actually are, or are you still pouring budget into the platforms that dominated last decade’s media plan? What do you think? Let me know in the comments.

Technically Entertaining is a weekly briefing on how gaming, technology, and entertainment are reshaping brand strategy for decision-makers at the world’s biggest brands. Next week, I’ll be giving a keynote at the iicon conference, where top executives across gaming, entertainment, sports, and brands come together to shape the world of consumer engagement. I’ll be sharing important insights from behind closed doors - so be sure to subscribe below to not miss out.